What Went Wrong With Babylon Health?

The Telehealth Startup, Formerly Valued as a 'Unicorn,' Faces Bankruptcy

Unicorns are Mythical Creatures

The London-based digital primary care provider once hailed as a unicorn, has reached the end of its tumultuous journey. The company has agreed to sell most of its assets to U.S.-based eMed Healthcare through a bankruptcy process, marking the end of an era for a company that was once valued at nearly $2 billion.

A Glimpse into Babylon's Past

Founded in 2013, Babylon Health pioneered an integrated primary care model that utilized remote patient monitoring and an AI-powered healthcare app for diagnosis and video appointments. They also offered a value-based care platform known as Babylon 360.

In 2021, Babylon made a significant move into the U.S. market, attracting attention with a SPAC (Special Purpose Acquisition Company) plan worth over $4 billion. This expansion allowed the company to distance itself from ongoing issues in its core business.

However, in the U.K., concerns about patient safety and corporate governance had been raised by clinicians for years. In 2021, it was revealed that a U.K. medical regulator had also been expressing these concerns. Despite these issues, Babylon continued to expand its business.

The Search for a Lifeline

By 2022, Babylon began to face challenges as it lost major contracts in its home market, including a contract with the NHS for the city of Wolverhampton (UK). The company's fortunes continued to deteriorate.

In 2023, Babylon began seeking a buyer, with Swiss health tech startup MindMaze showing interest. However, the acquisition talks were plagued by uncertainties, and Babylon's shares were delisted from the New York Stock Exchange during negotiations. The acquisition ultimately fell through in August.

Babylon then shifted its focus to finding buyers for its assets, putting its U.S. business in Chapter 7 insolvency.

The Financial Collapse

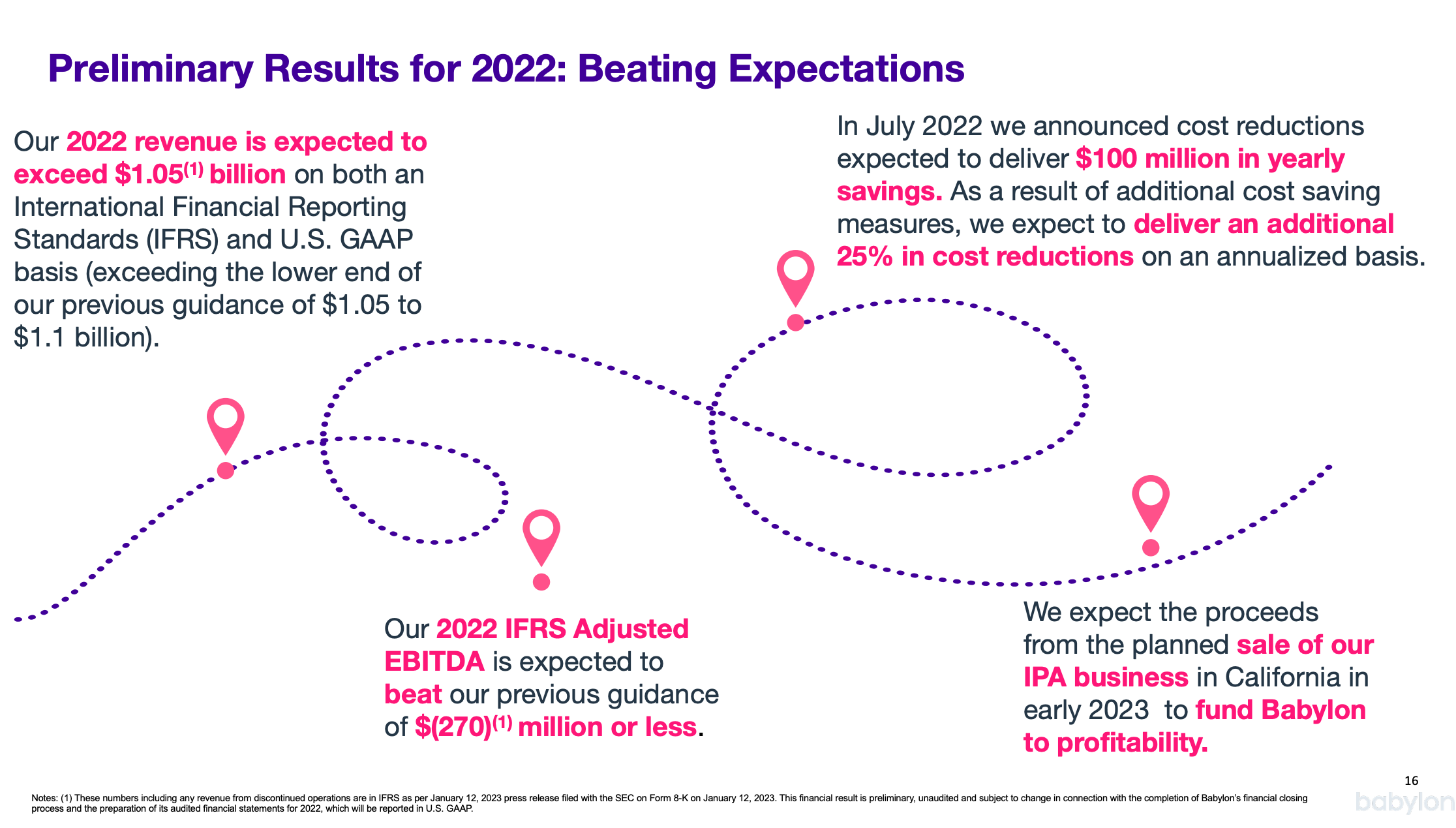

Babylon's rapid expansion in the U.S. market over 18 months came at a significant cost. The company reported a staggering net loss of $221 million on $1 billion in revenue in 2022. By May of the following year, its first-quarter losses had doubled compared to the previous year, reaching $63 million. These financial woes played a crucial role in Babylon's downfall.

While evaluating the business case, certain questions arose in my mind:

In what way could a healthcare company with assets scattered worldwide offer any form of lasting or enduring value?

Maintaining focus is exceptionally challenging in a world marked by irrational valuations and an abundance of capital, yet it remains absolutely essential.

What was the effectiveness of the acquisitions of Meritage Medical Network and First Choice Medical Group in 2021, with the intention of expanding in the USA, considering that 18 months later Babylon was seeking a buyer for the IPA business in California?

IPA is a network of approximately 1,800 physicians providing physical care in California. Babylon grew it from $111m in 2021 revenue to over $400m in estimated 2022 revenue.

The capability to acquire patients and quickly expand gross revenues should be counterbalanced by adeptly managing and controlling medical expenditures.

How trustworthy is it to present adjusted EBITDA margin in a business case involving a company like Babylon Health?

The adjusted EBITDA metric is particularly valuable when assessing a company's worth in various transactions, such as mergers, acquisitions, or fundraising efforts. For instance, if a company's valuation is based on an EBITDA multiple, the value could undergo substantial alterations following the inclusion of add-backs.

What's at stake in Babylon Health's situation? The primary risk lies in the nature of these adjustments, which typically encompass various types of expenses that are reintegrated into EBITDA. As a result, the resulting adjusted EBITDA often portrays an elevated earnings level due to the reduction in expenses.

eMed's Acquisition

eMed Healthcare has acquired most of Babylon Health's assets, and while the company's future plans remain uncertain, it is expected to keep the acquired business operational. eMed itself started as a startup and was backed by investors like Bessemer Ventures Partners, SV Health Investors, and Credit Suisse.

GP at Hand, an app and service powered by Babylon that can be selected by U.K. residents as their primary health practice, is not a part of the sale, nor was put through any insolvency process, a spokesperson said. It’s still operational. (According to the site, it appears that three partners — Dr. Stephen Jefferies, Dr. Matt Noble and Rita Bright — are the primary owners of it.)

The Broader Lesson

The demise of Babylon Health serves as a cautionary tale for investors and a reflection of the volatile nature of the digital health startup landscape. In today's funding environment, Babylon will likely not be the last digital health startup to falter. As the cost of capital and funding opportunities evolve, many of these companies, often operating without profitability or substantial revenue, may struggle to sustain themselves. Unicorn status can be fleeting, and the story of Babylon Health reminds us that even the most promising startups can face a harsh reality check.

+ Camels 🐫 startups are good,

Martin

P.S. I used some of the following sources to obtain the data for this article:

(1) TechCrunch (2) www.babylonhealth.com